December 17, 2020

Assessing the Emerging Threats From Innovation in the Automobile (Mobility) Industry

TL;DR

- First, we review the low variation in technological innovation amongst companies in the automotive (mobility) industry, in contrast to other industries.

- Second, we discuss the digital/exponential technologies underlying these opportunistic innovations.

- Finally, we present a brief analysis of emerging threats and risks to mobility companies due to the new innovations they are pursuing.

At the start of 2020, the Association of Global Automakers and the Alliance of Automobile Manufacturers announced a merger into what is now the unified Alliance for Automotive Innovation. Unlike some industries where technological innovation isn’t strictly necessary, it is ubiquitous in the automotive (AKA “mobility”) industry, from vehicle design to advanced manufacturing to tech-heavy dashboards.

Auto manufacturing companies largely move in lockstep with each other; in other words, they tend to work on the same features around the same time. There aren’t really companies who are five years behind on key features, or who steadfastly refuse to make their engines, dashboards, or safety features more modern (there are certainly regulatory and other reasons for why this is). They all pretty much keep up with each other technologically, and people make their purchasing decisions for other reasons – price, brand, design, and so forth.

This isn’t true in many other industries, where companies or industry segments have completely different business strategies and investment in technology. Take retail stores and restaurants, where some are very high-tech with regard to operations like tracking inventory or analyzing customer data, and others are fairly “old school” and could easily be run by time travelers dropped here from 1960. Within subgroups, there’s even variation – McDonald’s is arguably more high-tech than Burger King. At least subconsciously, consumers might choose one store or restaurant over a different, roughly equivalent one because service is faster, or the app has a better interface, or delivery is more predictable and reliable.

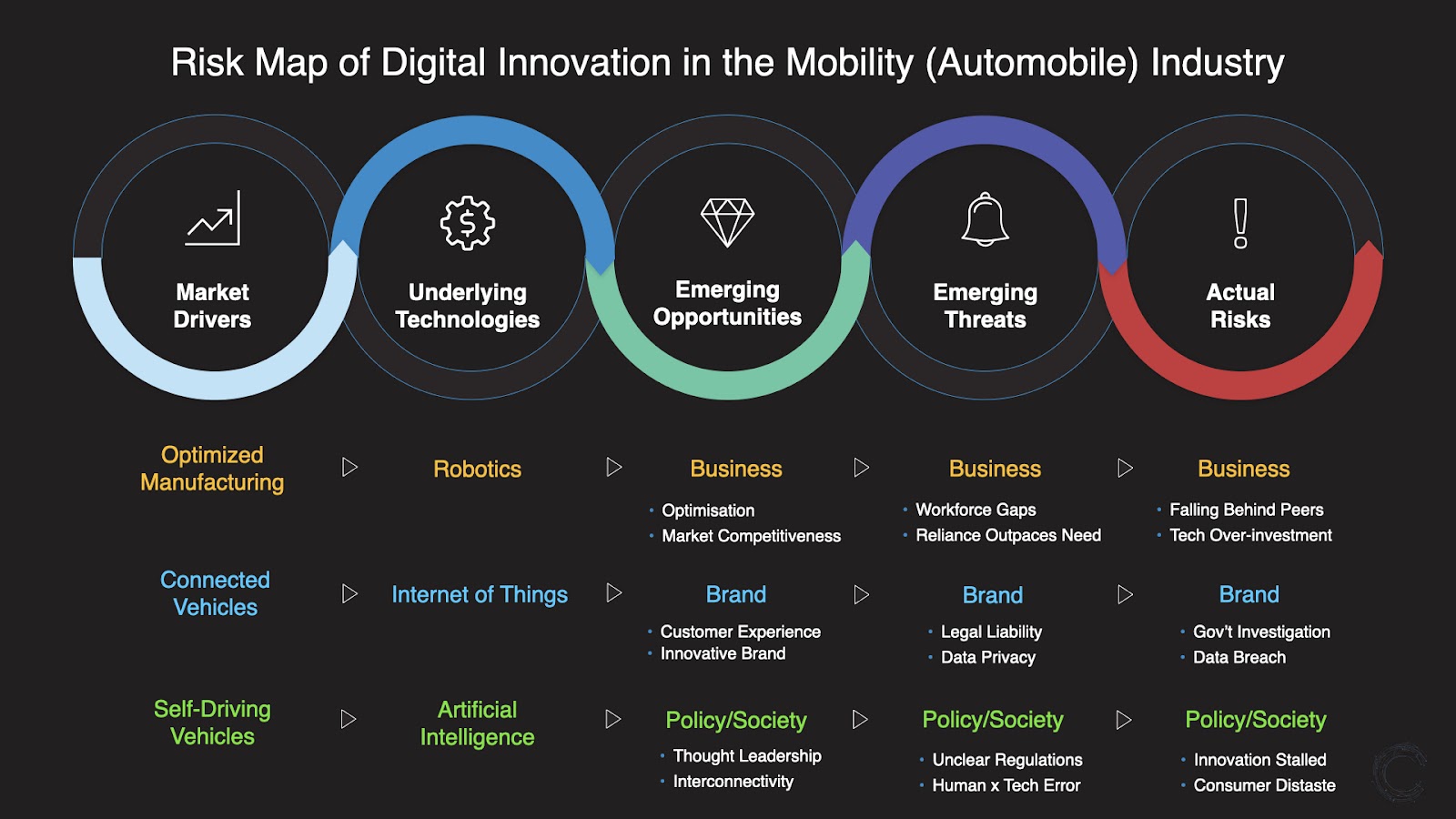

Why is there less variation in tech amongst mobility companies? In our view, the industry is currently aligned around three high-tech “market drivers” which largely define where the companies invest, innovate and evolve with regard to technology. Each of these drivers, in turn, are enabled by a number of underlying digital and/or “exponential” technologies for which critical expertise is required, namely the Internet of Things (IoT), Robotics & Automation, and Artificial Intelligence/Machine Learning (AI/ML). The three drivers are as follows:

Optimized Manufacturing: Vehicles are complex to manufacture, involving many vendors, parts, people, and tests. Obviously, optimizing this process through forms of automation and analysis saves companies time and money. While it may be under-the-radar for the average consumer, mobility companies have integrated advanced robots into their factories and actively promote their capabilities in this area.

Connected Vehicles: At a basic level, new vehicles are “smartphones on wheels,” incorporating digital dashboard interfaces, internet connectivity, device synchronization, and even sophisticated mobile apps into a relatively high-tech driver or passenger experience. Companies are also rolling out vehicle to vehicle communication, vehicle to infrastructure communication, and other IoT-related enhancements.

Self-driving Vehicles: While fully autonomous vehicles are in an experimental phase, current model vehicles often already possess low levels of autonomous features such as AI/ML-driven cruise control (whether you fully realize it or not). Underlying this kind of work is a major investment in big data analytics and cloud computing.

One aspect of our own in-house research on numerous industries quantifies a company’s “implementation level” across 10 digital/exponential technologies (including Robotics & Automation, IoT, and AI/ML). Using this proprietary data, we tested the hypothesis that because automobile manufacturers were in lockstep on technological innovation at a strategic level, this would be reflected as a lack of variation amongst them in how they have been deploying digital technologies across the company. Indeed, we found low variation for implementation level amongst 10 major automobile manufacturing companies (results not shown).

If mobility companies are broadly deploying digital technologies and strategically innovating their products and operations in lockstep, they are clearly doing this to take advantage of new and unique opportunities (see graphic). But that should beg the question: Do these new innovations create new “threat vectors” for companies that can result in company- or industry-level risks?

Across our proprietary framework of the potential opportunities, threats, and risks stemming from digital innovations, we assessed the most likely threat vectors and potential risks stemming from each of the three drivers above. While there are other potential scenarios, we believe these are the most likely ones that should be prepared for by strategy, communications, and government affairs professionals.

Optimized Manufacturing: The biggest potential risk from Optimizing Manufacturing is Business Risk from use of Robotics, which requires a high-skill, interdisciplinary workforce currently in short supply. As the mobility industry expands its optimized manufacturing, its need for qualified engineers will grow as well, and with a limited talent pool there are costs associated with recruitment and retainment, and also the risk that this won’t be successful to the degree needed. On the other hand, some companies might in fact find they are overinvested in automation vs. human talent, leading to different challenges in the business (Tesla experienced this). Maintaining business competitiveness without overinvesting is the key challenge.

Connected Vehicles: The biggest potential risk from Connected Vehicles is a Brand Risk from use of IoT. Because today’s connected cars have become a “rolling mass surveillance network with potentially millions of participating vehicles,” a massive amount of unregulated data is being generated every minute. Privacy considerations alone include the relatively undefined extent to which law enforcement can access this data legally, and hackers could access this data illegally. This backdrop puts mobility companies in the “hot seat” of potentially being at the core of dramatic privacy violations that could subsequently damage their brands.

Self-driving Vehicles: Finally, the biggest potential risk from Self-driving Vehicles is a Policy Risk from use of AI/ML. The question of how much, and at what point, we are going to put our trust in AI/ML in various situations (especially when human life is involved) is currently an open one. Self-driving vehicles have pushed this once-abstract concept to a more active conversation amongst legislators, regulators, and other stakeholders and influencers. The policy landscape between now and a future with autonomous vehicles is complex, and the risk of an uncertain regulatory environment and timeline creates a Policy Risk for mobility companies.

While we discuss these threats and risks in a somewhat abstract and disconnected manner above, these risks are not mutually exclusive, and they can already be observed in the real world. Take the case of Uber, which just sold off its Advanced Technologies Group (ATG) (i.e., self-driving cars) in December 2020 after feeling the effects of three threat vectors:

(1) Business Threat (Patent/IP Issues): legal entanglements with Waymo (part of Alphabet) about intellectual property

(2) Brand Threat (Physical Safety): the death of a pedestrian in Tempe, Arizona

(3) Policy Threat (Unclear Regulatory Environment): a complex policy landscape which confined this group’s on-road work to within a closed environment in Pittsburgh

With ATG already being a risky part of Uber’s business, the coronavirus pandemic crushed the unprofitable company financially which resulted in the divestiture of ATG, which was founded in 2015. The rise and fall of ATG under Uber (itself only a ~10 year old company) demonstrates the necessity of innovation to take advantage of strategic opportunities, the threats that arise precisely because of that innovation, and the rapid pace of change in the digital world.

Mark Drapeau is a Partner and Chief Research Officer of Catalyst Research. Ronit Langer assisted with the research described here.